(From Credit Union Times) – Credit unions gained share in a shrinking credit card market in September, while losing share in a slow-moving market for car loans, according to a Fed report released Wednesday.

The Fed’s G-19 Consumer Credit Report showed credit unions showed credit unions held $61 billion in credit card debt, down 5.2% from a year earlier. The change was a drop of 0.31% from Aug. 31 to Sept. 30, compared with a 0.2% gain from August to September in 2019.

Credit union’s share was 6.4% in September, down slightly from 6.5% in August but up from 6.2% in September 2019. The share rose as banks and finance companies had steeper drops.

Banks held $850.1 billion in credit card debt, down 9.2% from a year earlier. Banks’ share was 89.6% in September, compared with 89.5% in August and 89.6% in September 2019. Finance companies held $17 billion in credit card debt, down 27.3% from a year earlier.

The drop in credit card balances has continued for all lenders since COVID-19 was declared a pandemic March 11.

In February, credit card balances grew 3.5% for all lenders from a year earlier, but they fell 4.7% in April to dip below $1 trillion for the first time since July 2018. Since then drops have ranged from 7.3% in May to 9.5% in August. In September, balances fell 9.2% to $948.7 billion for all lenders.

Credit card balances have been falling at credit unions too, but at roughly half the rate of banks.

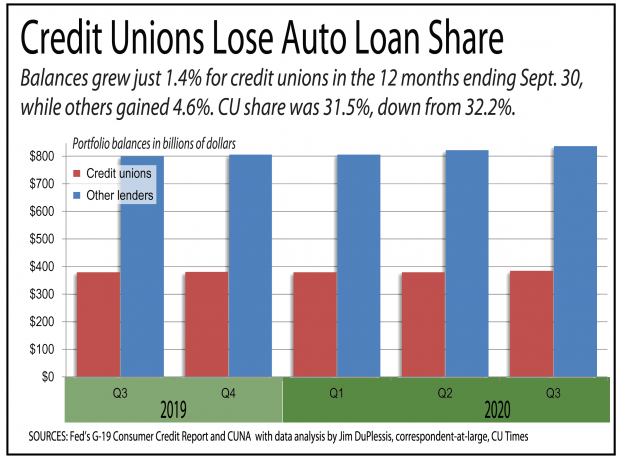

n motor vehicle lending, the G-19 shows all lenders held $1.22 trillion in loans in September, up 3.6% from a year earlier.

Comparing the Fed’s numbers with CUNA’s Monthly Credit Union Estimates released Thursday shows credit unions held 31.5% of the nation’s car loans on Sept. 30, down from 32.2% a year earlier and 31.6% as of June 30.

The Madison, Wis., trade group found credit unions held $385.5 billion in car loans as of Sept. 30, up just 1.6% from a year earlier. New auto loans fell 3.8% to $143.5 billion, while used auto loans rose 5% to $242 billion.

Banks and other lenders held $837.4 billion in car loans, up 4.6% from a year earlier.

CUNA and CUNA Mutual Group had predicted a significant slowdown in consumer and business loan growth, particularly auto loans.

In a CUNA Mutual Group report released Oct. 30, chief economist Steven Rick attributed the weak auto loan growth to “high economic uncertainty, low consumer confidence and cash-out refinances paying off new auto loan balances.”

Comparing CUNA and Fed reports shows unsecured consumer term loans at credit unions grew 14.3% to $52.8 billion as of Sept. 30. They grew 7.9% in the 12 months ending September 2019.

Besides its quarterly auto report, this month’s G-19 also showed government student loan balances rose 3.3% to $1.7 trillion. Student loans’ share of non-revolving loans was 53.3% in September, compared with 53.6% in September 2019.